{kind=link}

This is an exciting time for Africa. In early January 2021, the first shipments traded under Africa Continental Free Trade Area (AfCFTA) preferences left Ghana bound for Guinea and South Africa. Since its signing in March 2018, the rapid implementation of the agreement raises hopes of a more inclusive and prosperous future for the continent. How global trading partners support this project could set the tone of relationships for decades to come.

NEW TIMES REQUIRE A FRESH APPROACH…

The Biden administration is applying a healthy dose of fresh thinking to a number of Africa-relevant policy areas, from global taxation to intellectual property. In terms of trade, United States Trade Representative Ambassador Katherine Tai has already signaled a welcome new direction, stressing multilateral solutions over bilateral ones and emphasizing the importance of incorporating climate action in discussions on trade policy.

When it comes to U.S. trade with Africa, two linked items are on the agenda:

- The administration has inherited plans to negotiate a stand-alone free trade agreement (FTA) with Kenya. The new Biden administration initially announced a review of all trade negotiations started under President Trump, and, in April 2021, Secretary of State Antony Blinken confirmed that talks with Kenya would proceed.

- The Kenya agreement was conceived (by the Trump administration) as a blueprint for an FTA initiative designed to succeed the African Growth and Opportunity Act (AGOA), a trade preference scheme that has offered enhanced market access to qualifying African countries since 2000 but is due to expire in 2025.

For both geostrategic and economic reasons, the United States has a vested interest in ensuring the success of the AfCFTA and should avoid moves that might hinder that success. As the U.S. trade team weighs its options and fleshes out a new approach toward the African continent, we argue that, in light of the AfCFTA, bilateral FTAs with African countries should be reconsidered in favor of a continental approach. This recommendation chimes with the Biden administration’s preference for multilateralism and will, in turn, have implications for the future of AGOA.

For both geostrategic and economic reasons, the United States has a vested interest in ensuring the success of the AfCFTA and should avoid moves that might hinder that success.

THE UNDERLYING PROBLEM WITH FTAS BETWEEN AFRICAN AND HIGH-INCOME COUNTRIES

The European Union’s and United Kingdom’s experiences of trying to negotiate FTAs with countries or regions in Africa offer some useful lessons for the United States to consider.

The EU has been trying to secure economic partnership agreements (EPAs) with Africa for over two decades. In principle, these agreements were supposed to be signed on a regional basis, but because of disparate economic interests within regional blocks and concerns in Africa over the ability to compete with firms in the EU on a level playing field, the process was met with considerable reluctance by African partners. The EPAs offered no additional market access for least developed countries (LDCs)—and simply obliged those countries (albeit over a generous timeframe) to open their markets to the EU.

As a consequence, beyond a handful of single-country deals (Cameroon, Côte d’Ivoire, Ghana), just two regional deals were signed—one with East and southern Africa in 2009 and one with southern Africa in 2016. None of this messy patchwork of deals coincided with existing regional economic communities. The seed was thus sown for considerable difficulties in implementation. The EU itself has gradually shifted the discussion toward a different, arguably more accommodating, framework: the Africa-EU partnership.

To many commentators’ surprise, given the country’s post-Brexit political rhetoric, the U.K. missed a golden opportunity to chart a new course. Instead, for reasons of expediency and the desire to sign up quickly as many new trade deals as possible, it opted to roll over the unpopular EPA deals. This exercise has not proven at all straightforward and the newly inked U.K.-Kenya FTA faced hurdles in both the U.K. House of Lords as well as the Kenyan parliament. A legal case brought by small-scale farmers in Kenya is still pending.

On the part of African partners, bilateral deals have been seen as the product of necessity rather than forward-looking policy design. If we take the example of the U.K.’s deals with Kenya and Ghana, both countries are classified as “non-LDCs” and so, unlike neighboring countries in the East African Community (EAC) or Economic Community of West African States (ECOWAS), they do not qualify for the generous Everything But Arms preference scheme. The deals were signed not because they were seen as a gateway to accelerated export growth or diversification, but rather to protect existing market access for a handful of traditional, largely low value-add exports (flowers and vegetables for Kenya, bananas and tuna for Ghana).

FTAS BETWEEN COUNTRIES AT VASTLY DIFFERENT LEVELS OF DEVELOPMENT ARE RISKY

In a well-argued piece, Brodo and Opalo (2021) recently claimed that the U.S. should make deals with Africa’s regional economic communities (RECs), an intermediate solution between bilateral trade agreements and a U.S.-Africa continental trade agreement. This approach is certainly preferable to signing bilateral FTAs, but also presumes that all countries within a REC feel both ready and prepared to enter into an FTA with the world’s preeminent high-income, high-productivity economy. Arguably, this presumption was the underlying mistake made by the EU when it embarked on EPAs with the African continent nearly two decades ago.

In reality, Africa’s RECs contain countries with different economic priorities, interests, and levels of development. LDCs across the continent have been extremely reluctant to sign FTAs with developed economies for fear that their nascent domestic industries will not be able to survive the competition—particularly in sectors like agriculture where levels of domestic support in developed countries are high. The majority of countries on the continent already have to sustain major structural trade imbalances with high-income countries, and signing FTAs, even if the liberalization is gradual, is only likely to exacerbate those imbalances, entrenching patterns of dependence on low-value commodity exports.

In considering its new policy toward the African continent, the U.S. administration should also take fully on board the lessons to be learned from the Free Trade Area of the Americas (FTAA), a megaregional trade agreement over a broad range of countries with very different levels of development and economic structures, which ended ignominiously without agreement in 2005 after over a decade of negotiations (Herreros, 2019).

FTAS WITH SINGLE COUNTRIES UNDERMINE REGIONAL CUSTOMS UNIONS AND CREATE HEADACHES FOR ACFTA IMPLEMENTATION

Bilateral FTAs may be allowed under the terms of the AfCFTA, but this does not mean they are without cost. Regional-level customs unions such as that of the EAC and ECOWAS are extremely important building blocks toward wider continental trade integration. The practice of signing side deals with individual member states—especially if it becomes common practice—could undermine their common external tariffs and exacerbate division and tension.

Such side deals also complicate the implementation of the AfCFTA, which would lead to a heavy reliance on rules of origin to prevent trade deflection. It is also noteworthy that, as soon as its own customs union was formed in 1968, the EU no longer allowed member states to negotiate with third parties. Instead, in order to maintain internal coherence, the EU Commission took “exclusive competence” of external trade policy (Baldwin and Wyplosz, 2015).

THE CONTINENTAL ROUTE—THE PREFERRED AFRICAN OPTION

Looking to the future, countries like Ghana and Kenya seeking to grow their industrial bases and increase their share of manufactures in exports may consider pivoting away from a reliance on these oversaturated and mature developed-country markets that are often fickle and already dominated by powerful multinational companies.

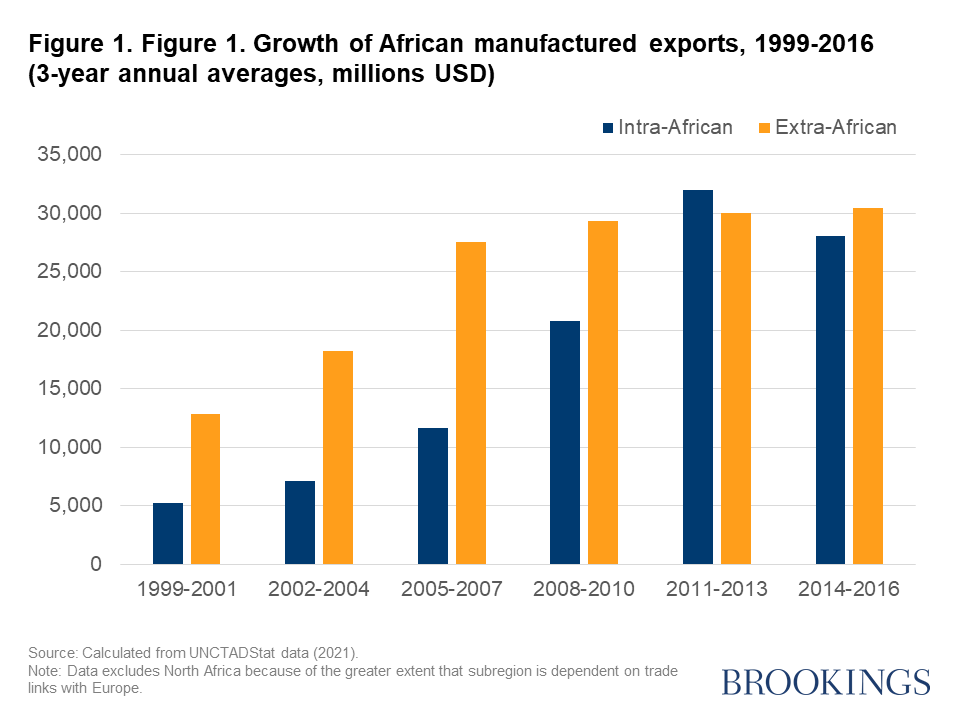

Instead, they should prioritize trade with the African continent through the AfCFTA, which, as UNECA Executive Secretary (and AGI Nonresident Senior Fellow) Vera Songwe (2019) observes, is much more likely to stimulate industrialization and much-needed creation of quality jobs. Despite the existence of preferential schemes to high-income markets like AGOA and the EU’s Everything But Arms, over the last two decades intra-African exports in manufactured goods have expanded by a factor of more than 5, much more rapidly than extra-African manufactured exports (Figure 1). By removing tariffs and reducing nontariff barriers on intra-African trade, the AfCFTA will provide a new impetus to this already ongoing process.

TOWARD A NEW US APPROACH TO TRADE RELATIONS WITH AFRICA

Rosa Whittaker, one of the architects behind AGOA, has recently claimed that:

“There is no appetite in Washington for AGOA’s unilateral trade benefits. In preparation for its 2025 expiration, AGOA needs to be renewed with smart trade reciprocity—pillar one. Some sectors have matured in specific countries thanks to AGOA and should, therefore, be considered for graduation from duty-free treatment.”

We beg to differ. AGOA has certainly proven to be an imperfect trade instrument: Outside fuels and minerals, the bulk of the export gains have accrued only to a small minority of countries, in a small range of industries—principally textiles. Nonetheless, at this juncture, that is no reason to adopt a “throw out the baby with the bathwater” approach and shift to fully reciprocal trade deals with Africa. The risk is that such policies will meet with the same resistance and opposition as the EU’s EPAs.

Instead of replicating the EU’s or U.K.’s flawed approaches, we argue that the Biden administration’s priorities would be better served by working with the African Union to design a fresh, forward-looking comprehensive partnership arrangement. An intermediate position would to be to start by addressing some of the flaws in existing AGOA market access (Laurence, 2013), and improving upon it—in other words, an updated, AGOA-style trade preference scheme made more predictable and with full continental cumulation in support of the AfCFTA. This policy would provide the necessary “breathing room” for Africa to consolidate its own process of regional integration first, after which a U.S.-Africa FTA could be explored.

This trade pillar could be embedded in a wider, new U.S.-African trade and development partnership that could include joint commitments on climate change and foreign and security policy, as well as ensure U.S. development support is coherent with Africa’s Agenda 2063 plans.

REVERSING THE RETRENCHMENT OF US ECONOMIC INTERESTS ON THE AFRICAN CONTINENT

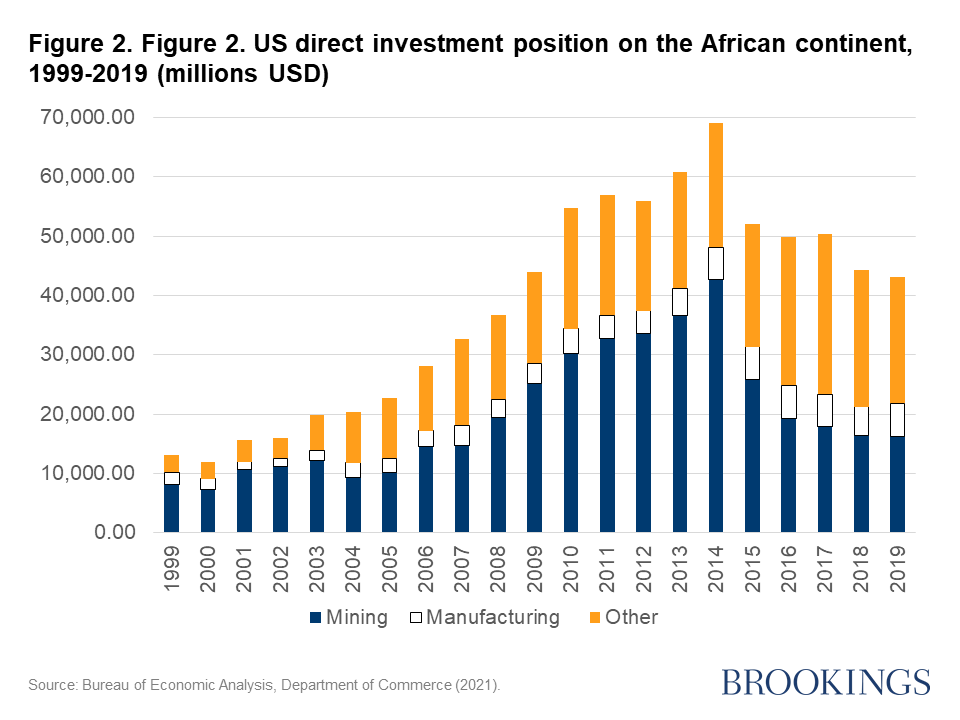

Finally, the U.S. has a long-term strategic interest in making sure that the AfCFTA is a success. The U.S. is a major investor on the African continent, and although foreign direct investment (FDI) stocks have been declining in recent years (principally because of low mineral and fuel prices globally, which have led to a degree of divestment in these sectors), in 2018, U.S. firms still held more than $44.4 billion in FDI stock in Africa, controlling assets worth $370 billion, making sales of $116.3 billion, and employing 370,000 people across the continent (U.S. Department of Commerce, 2021) (Figure 2). Yet, in recent years, China has been the most active investment partner, accounting for around double the estimated FDI flows to Africa compared with the United States (Madden, 2019).

The AfCFTA represents an opportunity to turn this trend around. Reflecting the vibrancy of the U.S. investor community on the continent, the U.S. has an extended system of chambers of commerce and business associations across 21 countries on the continent. Much as they did in Europe in the postwar period (Mold, 2000), U.S. firms could help act as cheerleaders to the AfCFTA, integrating their operations across borders and shifting the focus of their activities away from the extractive sector and toward higher-value added activities in services and manufacturing. Ford’s recent decision to invest $1 billion in its operations in South Africa is a sign of the confidence in the continental market. In aligning both its trade and investment policies toward Africa with the AfCFTA, the United States thus has a unique opportunity to support African unity and economic prosperity. It is an opportunity that should be seized.